Q4FY2019 Result Update | NBFC

May 25, 2019

Shriram Transport Fin Co

BUY

CMP

`1,106

Performance Highlights

Target Price

`1,470

Investment Period

12 Months

Particulars (` cr)

4QFY19

3QFY19

% chg (qoq) 4QFY18

% chg (yoy)

NII

1,906

2,027

-6.0

1,855

2.8

Sector

NBFC

Pre.Prov. Profit

1,512

1,620

-6.7

1,605

-5.8

Market Cap (` cr)

25,114

PAT

746

635

17.4

962

-22.4

Beta

1.4

Source: Company

52 Week High / Low

1559/903

For Q4FY2019, STFC reported subdued numbers, NII grew -6/3% and AUM grew

Avg. Daily Volume

39,722

by 1%/9% on qoq/yoy. The primary reason behind moderate growth in AUM was

Face Value (`)

10

lackluster real estate activity, slowdown in demand of CV as well as election period.

BSE Sensex

39,434

Provisions during the quarter were `540cr against `97cr in 4QFY2018.

Nifty

11,844

AUM growth moderated; pressure on NIM: During the quarter, STFC reported

Reuters Code

SRTS.NS

AUM growth of 9% yoy, led by working capital (61% yoy on low base) and business

Bloomberg Code

SHTF.IN

loan (14% yoy). The reported NIM declined 28bps yoy (22bps qoq), due to increase

in lower yield investment and higher disbursement towards at the end of quarter.

Shareholding Pattern (%)

The cost-income ratio increased 91bps yoy to 22.1% as the company continued

investment into manpower and branches during the year. Credit cost sequentially

Promoters

26.1

decreased 38bps to 2.07%, and management has given guidance of 2% credit cost

MF / Banks / Indian Fls

3.9

for FY2020.

FII / NRIs / OCBs

52.1

Indian Public / Others

17.9

On asset quality front, GNPA declined from 8.78% to 8.37% sequentially, while

NNPA decline from 5.86% to 5.49% qoq. Provision coverage ratio remained stable

at 70%. We expect GNPA/NPA to stabiles as the transition to 90dpd and Ind AS

Abs.(%)

3m 1yr 3yr

completes.

Sensex

8.9

13.8

55.8

Outlook & Valuation: We expect STFC’s AUM to grow at CAGR of 16% over

SHTF

0.8

(25.0)

(4.2)

FY2019-21E primarily owing to (1) post election government to increase spending

on infra project (macro recovery), and (2) pre-buying of CV before the BS VI will

also improve the pricing of older vehicles. We expect STFC to report RoA/RoE to

2.7%/17.6% in FY2021E respectively. At CMP, the stock is trading at 1.3x FY2021E

ABV and 7x FY2021E EPS, which we believe is reasonable for differentiated

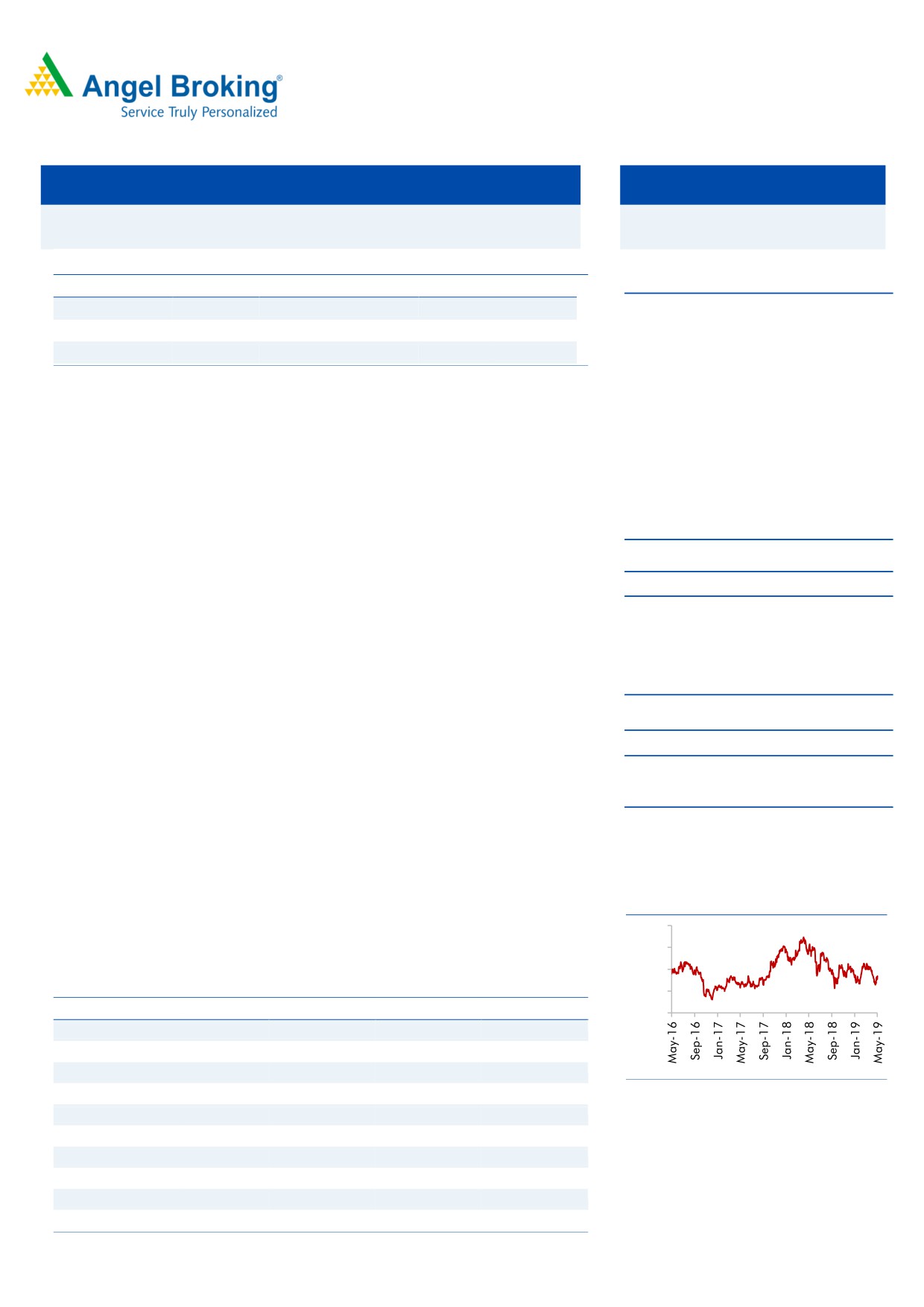

3-year price chart

business model with return ratios. We recommend a BUY on the stock with a Target

1800

Price of `1,470.

1500

1200

Exhibit 1: Key Financials

900

Y/E March (` cr)

FY18

FY19

FY20E

FY21E

600

NII

6,800

7,808

8,804

10,305

YoY Growth (%)

22.3

14.8

12.8

17.0

PAT

2,460

2,562

2,910

3,531

Source: Company, Angel Research

YoY Growth (%)

95.7

4.2

13.6

21.3

EPS

108

113

128

156

Adj Book Value

504

607

696

815

P/E

10

9

8

7

Jaikishan J Parmar

P/Adj.BV

2.1

1.7

1.5

1.3

Research Analyst

ROE (%)

19.8

17.4

17.0

17.6

022 39357600, Extn: 6810

ROA (%)

2.9

2.5

2.6

2.7

Source: Company, Note: CMP as of 25/05/2019

Please refer to important disclosures at the end of this report

1

Shriram Transport Fin Co | 4QFY2019 Result Update

Exhibit 1: Quarterly Summary

Particular (` cr)

4QFY18

1QFY19

2QFY19

3QFY19

4QFY19

% QoQ

% YoY

Total Interest Income

3,572

3,732

3,917

3,968

3,845

(3)

8

Interest Expenses

1,717

1,851

1,862

1,941

1,939

(0)

13

Net Interest Income (NII)

1,855

1,881

2,055

2,027

1,906

(6)

3

Other Income

173

7

24

26

35

34

(80)

Total Income

3,745

3,740

3,942

3,994

3,880

(3)

4

Net Income

2,028

1,888

2,080

2,053

1,941

(5)

(4)

Operating Expenses

423

472

458

433

429

(1)

1

Employee Expenses

206

225

232

222

204

(8)

(1)

Other Operating Expenses

217

247

226

211

225

6

4

Operating Profit

1,605

1,416

1,622

1,620

1,512

(7)

(6)

Provisions

97

533

684

636

540

(15)

455

PBT

1,508

883

938

984

972

(1)

(36)

Provisions for Tax

546

310

329

348

226

(35)

(59)

Tax Rate %

36

35.1

35.1

35.4

23.3

(34)

(36)

PAT

962

573

609

635

746

17

(22)

Profitability

C/I

21.2

25.0

22.0

21.1

22.1

101

91

ROE

4.6

17.2

17.0

17.2

19.4

217

1,472

Calc -Yield - AUM

14.05

15.25

15.29

15.25

14.77

(48)

72

Calc -Yield - Advance

16.89

18.42

18.40

18.42

18.13

(28)

124

Reported NIM

7.5

7.44

7.52

7.44

7.22

(22)

(28)

Calc - COF

8.3

9.97

8.59

8.74

8.74

0

42

Spread

8.6

8.5

9.8

9.7

9.4

(29)

83

Source: Company, Angel Research

Exhibit 2: Asset Quality

Particular (` cr)

4QFY18

1QFY19

2QFY19

3QFY19

4QFY19

% QoQ

% YoY

GNPA

7,376

7,459

7,749

7,641

7,100

(7)

(4)

NNPA

2,131

2,132

2,278

2,221

2,055

(7)

(4)

Gross NPAs (%)

9.15

8.98

8.77

8.97

8.29

(68)

(86)

Net NPAs (%)

2.83

2.74

2.75

2.78

2.55

(23)

(28)

PCR (Calculated, %)

69

69

69

69

69

23

17

Credit Cost (Annualised) AUM

0.4

2.1

2.6

2.5

2.1

(38)

166

GS 3

9,084

9,157

9,092

9,033

8,623

(5)

(5)

GS 3 %

9.5

9.1

8.7

8.7

8.3

(5)

(13)

ECL prov stage 3

3,286

3,118

3,113

3,187

2,967

(7)

(10)

Net Stage 3

5,799

6,039

5,979

5,846

5,656

(3)

(2)

Coverage Ratio Stage 3

36

34

34

35

34

(87)

(179)

GS 1& 2

87,617

91,879

96,173

93,875

94,358

1

8

ECL Prov stage 1& 2

2,364

2,341

2,604

2,651

2,604

(2)

10

Net Stage 1 & 2

85,253

89,538

93,568

91,224

91,755

1

8

ECL Prov (%) Stage 1&2

2.70

2.55

2.71

2.82

2.76

(6)

6

Source: Company, Angel Research

May 25, 2019

2

Shriram Transport Fin Co | 4QFY2019 Result Update

Exhibit 3: AUM Break-up

Particular (` cr)

4QFY18

1QFY19

2QFY19

3QFY19

4QFY19

% QoQ

% YoY

New

11,042

12,140

12,719

12,077

11,594

(4)

5

Used

80,784

83,919

86,057

86,126

87,050

1

8

Business Loan

2,611

2,978

3,314

3,182

2,971

(7)

14

Working Capital

1,741

1,895

2,171

2,365

2,807

19

61

Others

81

46

119

68

60

(12)

(26)

Total AUM

96,260

1,00,978

1,04,380

1,03,818

1,04,482

1

9

Source: Company, Angel Research

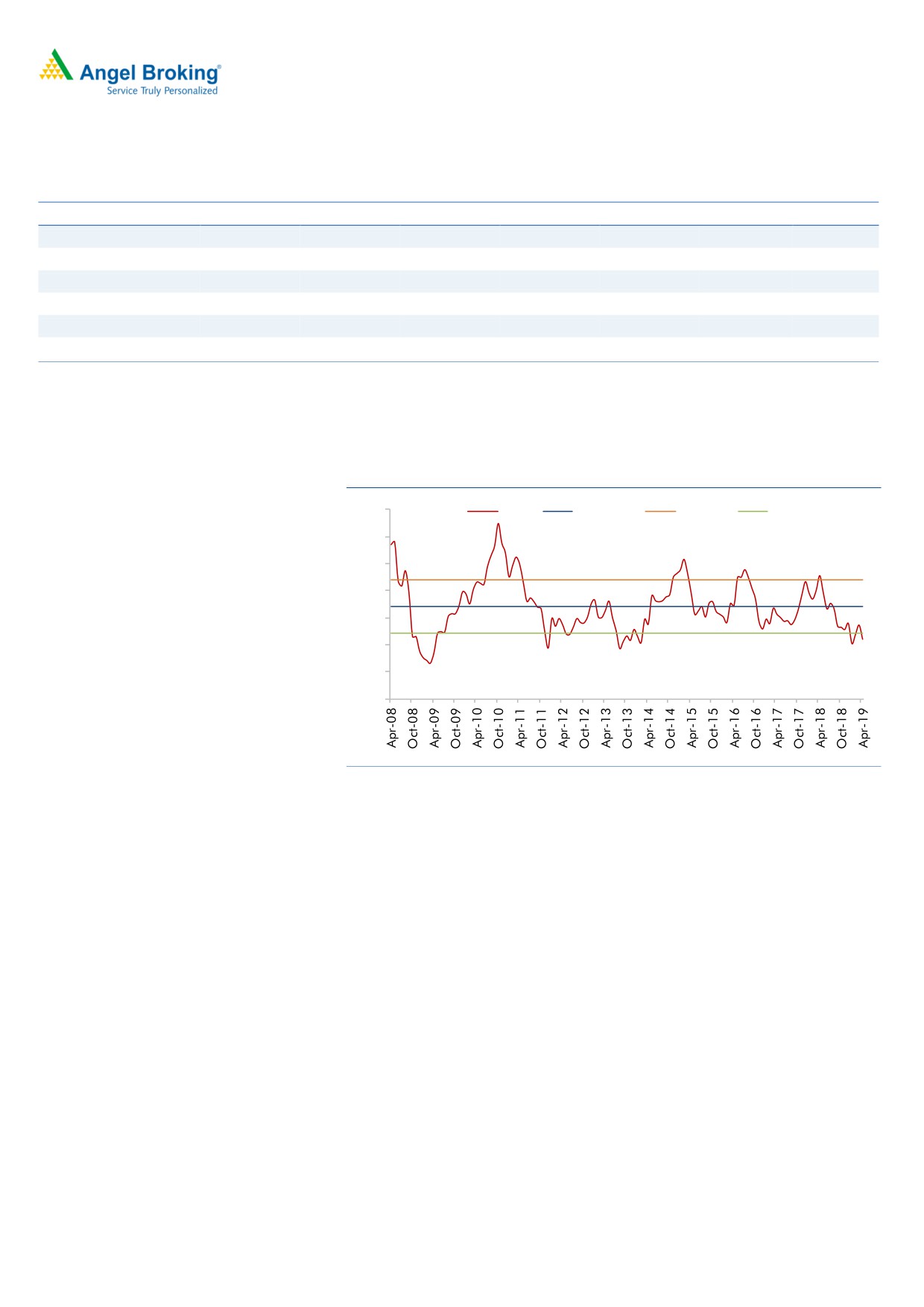

Exhibit 4: 1 year forward P/B

4

P/BV

Avg. P/BV

+1STD

-1STD

3.5

3

2.71

2.5

2.21

2

1.5

1.71

1.6

1

0.5

Source: Company, Closing rate as on 23/5/19

Outlook & Valuation: We expect STFC’s AUM to grow at CAGR of 16% over

FY2019-21E primarily owing to (1) post election government to increase spending

on infra project (macro recovery), and (2) pre-buying of CV before the BS VI will

also improve the pricing of older vehicles. We expect STFC to report RoA/RoE to

2.7%/17.6% in FY2021E respectively. At CMP, the stock is trading at 1.3x

FY2021E ABV and 7x FY2021E EPS, which we believe is reasonable for

differentiated business model with return ratios. We recommend a BUY on the

stock with a Target Price of `1,470.

May 25, 2019

3

Shriram Transport Fin Co | 4QFY2019 Result Update

Income Statement

Y/E March (` cr)

FY18

FY19

FY20E

FY21E

NII

6,800

7,808

8,804

10,305

- YoY Growth (%)

22.3

14.8

12.8

17.0

Other Income

215

101

113

130

- YoY Growth (%)

162.8

-53.0

11.4

15.5

Operating Income

7,015

7,909

8,916

10,435

- YoY Growth (%)

24.3

12.7

12.7

17.0

Operating Expenses

1,492

1,750

2,023

2,346

- YoY Growth (%)

17.0

17.3

15.6

15.9

Pre - Provision Profit

5,524

6,159

6,893

8,089

- YoY Growth (%)

26.4

11.5

11.9

17.3

Prov. & Cont.

1,722

2,382

2,484

2,739

- YoY Growth (%)

-29.5

38.3

4.3

10.3

Profit Before Tax

3,801

3,776

4,409

5,350

- YoY Growth (%)

97.6

-0.7

16.7

21.3

Prov. for Taxation

1,341

1,214

1,499

1,819

- as a % of PBT

35.3

32.1

34.0

34.0

PAT

2,460

2,562

2,910

3,531

- YoY Growth (%)

95.7

4.2

13.6

21.3

Balance Sheet

Y/E March (` cr)

FY18

FY19

FY20E

FY21E

Share Capital

227

227

227

227

Reserve & Surplus

13,349

15,609

18,224

21,397

Net worth

13,576

15,836

18,451

21,623

Borrowing

82,131

87,968

1,00,284

1,16,329

- YoY Growth (%)

54.6

7.1

14.0

16.0

Other Liab. & Prov.

1,539

1,487

1,821

2,351

Total Liabilities

97,245

1,05,291

1,20,556

1,40,304

Investment

2,341

3,999

3,999

3,999

Cash

3,675

3,981

4,680

5,432

Advance

90,738

96,751

1,11,264

1,30,178

- YoY Growth (%)

38.6

6.6

15.0

17.0

Fixed Asset

120

147

154

162

Other Assets

383

413

458

532

Total Asset

97,257

1,05,291

1,20,556

1,40,304

Growth (%)

30.7

8.3

14.5

16.4

May 25, 2019

4

Shriram Transport Fin Co | 4QFY2019 Result Update

Exhibit 5: Key Ratio

Y/E March

FY18

FY19

FY20E

FY21E

Profitability ratios (%)

NIMs

8.5

8.1

8.2

8.3

Cost to Income Ratio

21.3

22.1

22.7

22.5

RoA

2.9

2.5

2.6

2.7

RoE

19.8

17.4

17.0

17.6

Asset Quality (%)

Gross NPAs (%)

9.15

8.3

8.0

7.5

GNPA Amt

7,376

7,100

8,901

9,763

Net NPAs

2.83

2.6

2.4

2.4

NPA Amt

2,131

2,055

2,670

3,124

Provision Coverage

69.1

69.2

70.0

68.0

Credit Cost (AUM)

1.8

2.3

2.1

2.0

Per Share Data (`)

FY18

FY19

FY20E

FY21E

EPS

108

113

128

156

ABVPS

504

607

696

815

DPS

11

11

13

16

BVPS

598

698

813

953

Valuation Ratios

PER (x)

9.7

9.3

8.2

6.8

P/ABVPS (x)

2.1

1.7

1.5

1.3

P/BVPS

1.8

1.5

1.3

1.1

Dividend Yield

1.0

1.1

1.2

1.5

DuPont Analysis

FY18

FY19

FY20E

FY21E

NII

7.9

7.7

7.8

7.9

(-) Prov. Exp.

2.0

2.4

2.2

2.1

Adj. NII

5.9

5.4

5.6

5.8

Other Inc.

0.3

0.1

0.1

0.1

Op. Inc.

6.2

5.5

5.7

5.9

Opex

1.7

1.7

1.8

1.8

PBT

4.4

3.7

3.9

4.1

Taxes

1.6

1.2

1.3

1.4

RoA

2.9

2.5

2.6

2.7

Leverage

6.9

6.9

6.6

6.5

RoE

19.8

17.4

17.0

17.6

Valuation done on closing price of 24/5/19

May 25, 2019

5

Shriram Transport Fin Co | 4QFY2019 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER:

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National

Commodity & Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and

Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for

accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-

managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any

investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this

document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in

the securities of the companies referred to in this document (including the merits and risks involved), and should consult their

own advisors to determine the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions

and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a

company's fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our

website to evaluate the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other

reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as

such, as this document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be

in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information

contained in this report. Angel Broking Limited has not independently verified all the information contained within this

document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy,

contents or data contained within this document. While Angel Broking Limited endeavors to update on a reasonable basis the

information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be

reproduced, redistributed or passed on, directly or indirectly.

Disclosure of Interest Statement

Shriram Transport Fin

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

May 25, 2019

6